Employer Strategies

SmithRx

Key Takeaways

Bundled health plans lock employers into opaque, high-cost carrier ecosystems.

Modern health tech allows carved-out PBMs to integrate seamlessly with medical carriers.

Flat PMPM fees align PBM incentives to focus on the lowest-net-cost medications.

For years, the bundled medical and pharmacy plan has been viewed as the security blanket of corporate benefits. These plans are marketed as “one bill, one vendor”, but this conflates simplicity with efficiency. In 2026, with pharmacy costs firmly cemented as the fastest-growing expense for most employers, that simplicity has become a costly illusion.

When your pharmacy benefits are carved-in to your medical plan, they don’t just fall into a convenient line item. They potentially become lost within an insurance black box. You can lose critical visibility into how rebates are applied, how drug prices are set, and whether you’re actually saving.

‘Simplicity’ without control can be just a cleverly disguised trap for your business. Let’s explore how unbundling and moving to a self-insured plan can offer much-needed transparency and dramatically reshape your benefits for the better.

The Carrier Lock-In Trap: Why ‘Simplicity’ Curbs Your Leverage

When you select a bundled plan, you’re buying into a closed ecosystem. Some insurers, or medical carriers, may subtly suggest that unbundling would lead to administrative chaos or higher costs down the line.

When you lock your plan into bundled health and pharmacy benefits, it effectively diminishes your procurement leverage in a few key ways:

By bundling, the carrier removes your ability to shop for pharmacy rates in a competitive marketplace

If your carrier owns the PBM that’s bundled, they profit twice. This vertical integration creates a system where they have no incentive to point you toward the lowest net cost drug. Often, bundled, legacy PBMs direct patients towards high-list-price drugs manufactured and dispensed by subsidiaries and make additional profit off of the spread price.

As an employer, it’s in your best interest to choose best-in-class components for your benefits plan. Settling for a ‘default’ PBM is essentially leaving your second-largest cost driver to chance.

Debunking the Scalability and Interoperability Myths

A common scare tactic used to keep employers in bundled plans is the threat of integration headaches. Some carriers may claim that carving out pharmacy benefits will lead to disjointed member experiences, data silos, and an overall logistics nightmare for HR and benefits teams.

In our current age of technology and interconnectivity, this simply isn’t true.

Modern health tech has moved past the era of proprietary silos, even at enterprise scale. Modern PBMs, like SmithRx are designed from the ground up with flexibility, or interoperability, in mind. This means that they can integrate with any major medical carrier, or other benefits point solution, seamlessly.

SmithRx has built upon a solid foundation of technology, and continues to invest in it, to maximize our interoperability with best-in-class benefits providers and solutions. This is achieved through real-time data sharing via secure, standardized APIs. Information gets instantly passed from PBMs to TPAs, care partners, and navigators and vice versa, for a truly interconnected experience.

Unbundling benefits doesn’t mean benefits teams need to wrangle several benefits providers and members need to carry around countless benefits cards either. Integrated digital care platforms ensure that carved-out benefits still feel fully inclusive to members once they reach the pharmacy counter.

This means your members get the same "seamless" feel, while your benefits and finance teams get unprecedented visibility into pharmacy spend.

Bundled Hidden Margins: How Black Box Models Drain Savings

In a bundled contract, ‘savings’ are often the result of a financial shell game. Carriers and legacy PBMs have mastered the art of appearing to save you money in the form of massive discounts, while actually retaining rebates and making profit off of spread. When pharmacy benefits are buried inside a medical premium, you aren't just paying for drugs. In reality, you’re paying for the carrier’s margin, hidden behind layers of opaque contractual language.

Where does your budget go? There are a few primary ways bundled structures divert savings away from your plan:

Spread Pricing

In a bundled model, you may not get the opportunity to ‘check under the hood’ to see how your PBM truly operates. This potentially allows for bad practices, like spread pricing, to run rampant. Spread pricing occurs when the PBM charges your plan one price for a drug (say $100) but pays the dispensing pharmacy a lower price (say $60). The PBM pockets the $40 ‘spread’ as pure profit.

If you lack claim-level transparency in your bundled plan, you may never see the $60 transaction; you may only see the final cost of $100. Over thousands and thousands of claims, this hidden margin can add massive, un-auditable expenses for your plan.

Rebate and Discount Promises

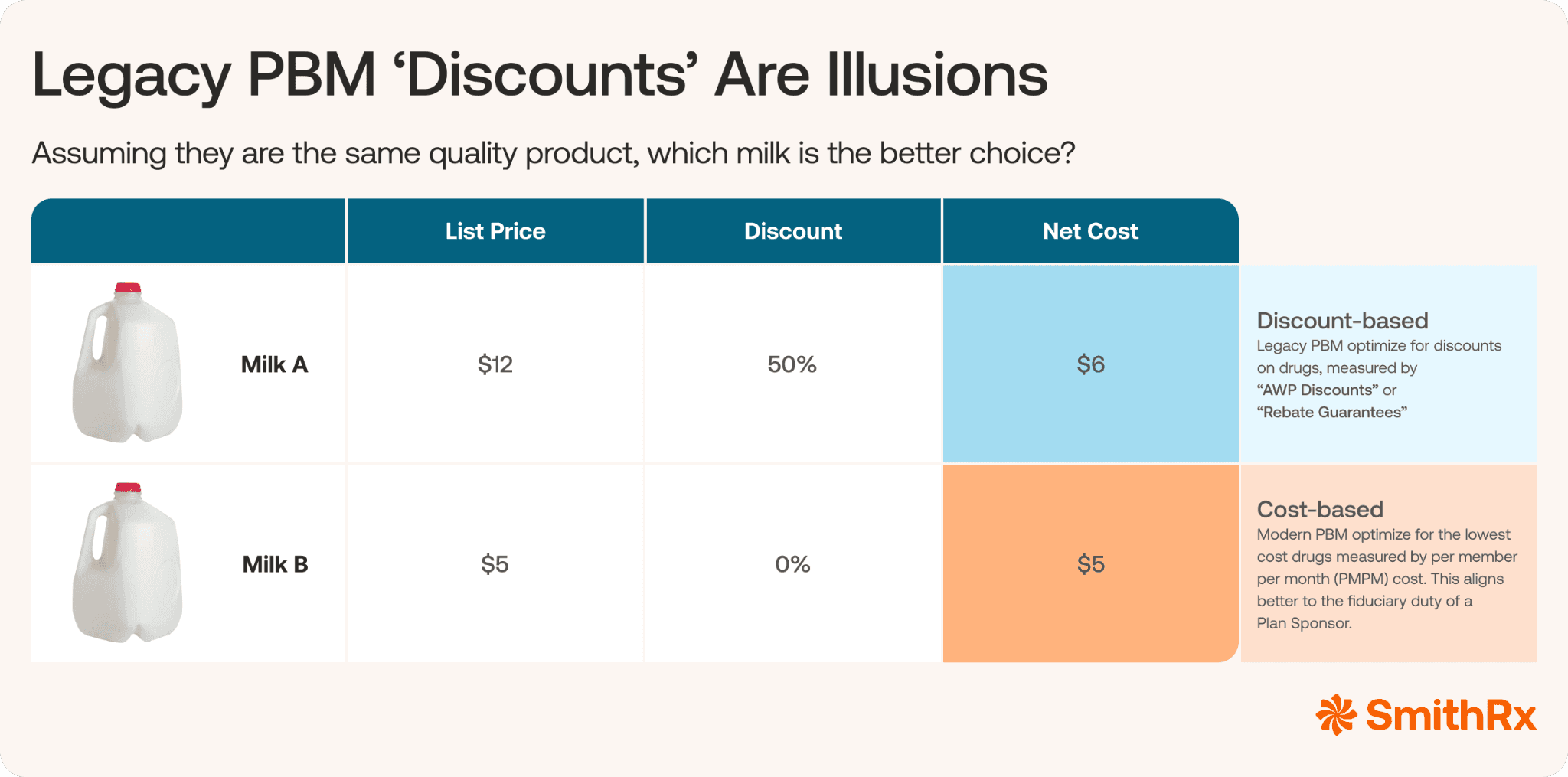

Many legacy PBMs boast large discount and rebate guarantees. This may look great in theory, but the math doesn’t add up to real value for your plan. Bundled models can be the ultimate black box where discounts are manipulated to solely suit the interest of the PBM.

When your true medication cost is hidden behind a curtain of carrier lock-in, a 50% discount on a 200% markup is still a bad deal for your plan.

This intense focus on discounts and rebates acts as a barrier to real savings; it creates a rebate trap where the PBM potentially avoids lower-cost options. The lowest-net-cost option often doesn’t provide the same opportunity for hidden profits and may not be sourced from an affiliated pharmacy or manufacturer.

Percentage-based vs. Platform-based Pricing Models

Bundled PBMs can potentially make money when your drug prices rise or when more expensive alternatives are used. This creates a fundamental conflict of interest: why would a PBM push for a lower-cost option if their contract allows them to take a percentage of a high-cost drug’s price?

At SmithRx, we believe that a PBM’s interests should be aligned with the plan’s. We operate on a flat, per member per month (PMPM) administrative fee. This platform-based pricing model means that:

SmithRx doesn’t make money off of pushing higher-priced drugs

SmithRx doesn’t make money if utilization goes up

Our incentives are 100% aligned with yours: to execute the lowest-net cost for the plan

The bundled myth relies on the idea that employers are too busy or too overwhelmed to look under the hood. But as a self-insured entity, you are a fiduciary. Managing your pharmacy spend is a core financial responsibility of your business.

You don't have to blow up your entire benefits package to see real results. You can keep your medical network, keep your carrier, and replace the PBM. Don’t let the ‘simple’ option cost you millions. Break the black box, demand claim-level transparency, and find a true PBM partner that’s aligned with your goals.

Want to make a change and upgrade your PBM to find a modern, cost-focused partnership? Check out our Ultimate Pharmacy Benefit Manager Evaluation Guide to discover how to run your next RFP to optimize for modernity.

SmithRx

SmithRx is the #1 Modern PBM, relentlessly focused on eliminating the conflicts and complexity of legacy pharmacy benefits. Built on radical transparency and fiduciary alignment, we empower employers to take control of their pharmacy spend and experience with our 100% pass-through model.