Modern PBM

SmithRx

Key Takeaways

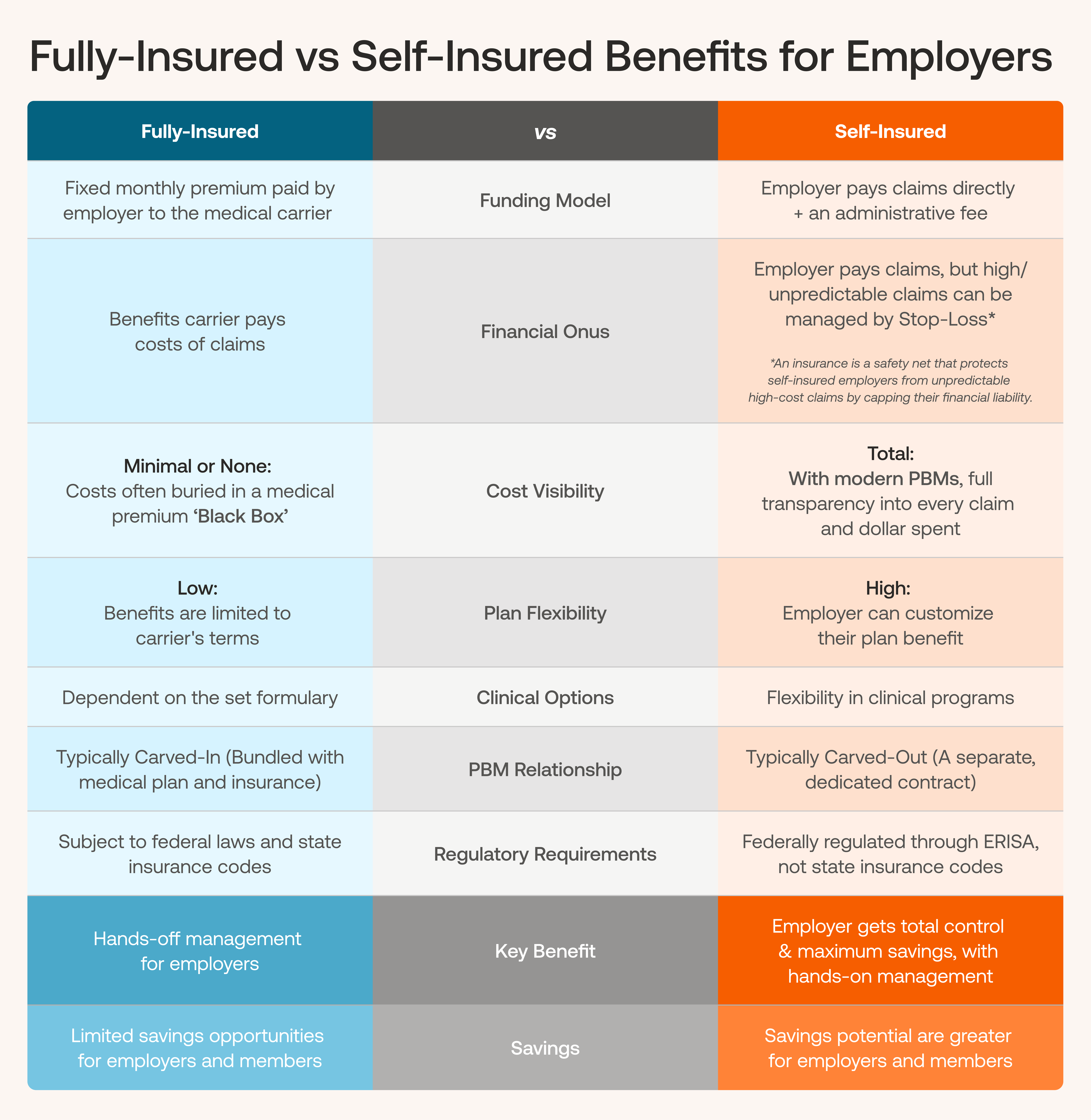

Fully-insured plans hide pharmacy costs inside premiums, giving predictability but little transparency or negotiating power.

Self-insured carve-out with a separate PBM restores visibility, flexibility, and direct savings: you fund claims, access detailed data, and use stop-loss to cap catastrophic risk.

Pharmacy costs are a top concern for employers, often the second-highest healthcare expense after hospital care. Yet, many organizations don't realize they can take direct control over these costs. The structure of your pharmacy benefit—how it's funded and whether it’s bundled with medical or managed separately—can be the difference between being locked into rising premiums and having real power to manage your spending.

At SmithRx, we work with employers who want that control. To understand why a self-insured, carve-out model is the best approach, let’s compare the options.

Fully-Insured: A Predictable, But Costly, Illusion

Many employers start with a fully-insured plan. In this model, you pay a fixed monthly premium to a health plan carrier, and they take on the financial risk of covering medical and pharmacy claims. This arrangement feels simple: one premium, one vendor, one contract. For small employers, that simplicity can be appealing.

But here’s the catch: pharmacy costs are buried inside the medical premium. You lose all visibility into what’s being spent on prescriptions, how rebates are applied, or if there are better, lower-cost options for your members. The carrier holds all the power, and you’re left with no control.

Fully-insured coverage can be a reasonable starting point, but as pharmacy costs rise, most employers eventually hit the same frustration: predictability without control is not sustainable.

Self-Insured: True Visibility and Flexibility

With a self-insured model, you pay claims directly and contract with vendors like a TPA (Third-Party Administrator) and a pharmacy benefit manager (PBM) to manage administration. Instead of a fixed premium, you fund the actual claims plus an administrative fee.

This model delivers powerful advantages:

Complete visibility into claims data and how every pharmacy dollar is spent.

Total flexibility to design a plan that fits your workforce, not the carrier’s rigid template.

Direct savings that flow back to you, rather than subsidizing a carrier's profit margin.

While self-insuring involves more financial risk from large, unexpected claims, this risk is easily managed with stop-loss coverage. What you gain is control—the ability to see, understand, and act on the factors driving your pharmacy spend.

What Is Stop-Loss Coverage?

While self-insuring offers greater control, it also means shouldering the financial risk of high-cost claims. Stop-loss insurance acts as a safety net, protecting employers from catastrophic or unpredictable losses. It's a key tool that allows employers to enjoy the benefits of self-funding without having to assume 100% of the liability for large, unexpected claims.

There are two main types of stop-loss coverage:

Specific Stop-Loss: This protects you from a single, high-cost claim from any individual employee.

For example, if your specific stop-loss limit is $50,000 and one employee incurs $100,000 in medical bills, the insurance would reimburse you for the $50,000 that exceeds your limit. It’s a safeguard against high-cost events like major surgeries or a serious illness.

Aggregate Stop-Loss: This provides a financial ceiling on the total amount you’ll pay for all claims across your entire employee population over a set period. If the total claims for the year exceed that predetermined threshold, the insurer reimburses you for the excess amount.

Here’s an example: imagine you have 100 employees and your aggregate stop-loss limit is set at $125,000. During the year, you project that your total claims will be around $100,000, but a flu outbreak, a series of minor accidents, or an unusually high number of claims pushes your actual total claims to $150,000. In this case, your stop-loss policy would reimburse you for the $25,000 that exceeded your aggregate limit, protecting you from a major financial hit.

By combining these two types of coverage, a self-insured employer effectively caps their financial risk while retaining all the benefits of control and transparency. This is how self-insuring becomes a good business decision, even for smaller employers who may not have a large financial cushion to absorb unexpected costs. It removes the perception that self-funding is too risky, making it a viable and powerful strategy for managing healthcare benefits.

Carve-In vs. Carve-Out: Where Pharmacy Lives

Once you’ve chosen a funding model, you have another critical decision: should pharmacy benefits be bundled with medical (carve-in) or managed separately by a PBM (carve-out)?

Carve-In (Bundled)

When pharmacy is carved in, it stays within the medical plan. You deal with one vendor and one bill, which appears simple. However, this simplicity comes at the expense of transparency. Drug pricing, rebates, and utilization trends are obscured within the carrier’s reporting. You lose the ability to negotiate pharmacy-specific contract terms, and your plan design is typically limited to what the carrier offers.

Carve-Out (Separate PBM)

In a carve-out model, pharmacy benefits are managed through a separate PBM contract. This adds a vendor relationship, but it creates powerful advantages:

Transparency into every claim and rebate.

Direct negotiating power specific to pharmacy benefits.

Flexibility to implement innovative clinical programs that directly serve your workforce.

In our experience, carve-out consistently delivers greater value. Pha rmacy benefits are too complex and costly to be just a line item in a medical contract. They require dedicated expertise, and a carve-out model ensures you get it.

The Only Model That Works: Self-Insured + Carve-Out

When you combine these choices, the best path forward becomes clear. Self-insured + carve-out is the gold standard. It gives employers the transparency, flexibility, and negotiating power they need to manage pharmacy spend effectively.

Here’s why this model wins:

Transparency: You see exactly what's being spent and where every dollar goes. There are no black boxes or hidden margins.

Flexibility: You can tailor your formulary, network, and clinical programs to fit your unique workforce and financial goals.

Accountability: Your PBM partner is directly responsible for performance, and you have the data to measure their impact.

We built SmithRx to be the modern PBM for this model. Our approach is radically transparent and fully fiduciary-aligned, designed to deliver results, not just reports.

How SmithRx Delivers

100% Pass-Through: Every rebate and discount flows directly back to you. Our only revenue is a transparent per-member-per-month administrative fee.

Fiduciary Alignment: We eliminate conflicts of interest. Our incentives are fully aligned with yours, ensuring every decision is made in the best interest of you and your members.

Drug Pathways Engine: Our proprietary technology continuously routes every prescription to the lowest net-cost, clinically appropriate option.

High-Touch Service: Our in-house teams simplify pharmacy benefits for everyone with short call wait times, fast prior authorization turnaround, and dedicated support.

Consistent Model: Every employer, regardless of size, gets the same contract terms, the same visibility, and the same aligned incentives. We don't cross-subsidize better deals for some clients by overcharging others.

Putting Employers Back in Control

Pharmacy benefits are too important—and too costly—to leave buried inside a medical premium. While fully-insured coverage may be a reasonable starting point, it limits the transparency and control you need at a time when costs are climbing fastest.

For employers ready to take ownership of their pharmacy spend, the self-insured carve-out model delivers true visibility, flexibility, and accountability. SmithRx is the PBM designed for this model: radically transparent, fully aligned with your fiduciary responsibility, and relentless about turning opportunities into real savings.

Ready to explore how a self-insured carve-out model can work for your organization? Get connected with one of our pharmacy benefits experts to begin your journey to a financially sustainable, self-funded future.

SmithRx

SmithRx is the #1 Modern PBM, relentlessly focused on eliminating the conflicts and complexity of legacy pharmacy benefits. Built on radical transparency and fiduciary alignment, we empower employers to take control of their pharmacy spend and experience with our 100% pass-through model.